Form 1099-INT Instructions & Tax Reporting Pointers

Form 1099-INT is an IRS information return used to report interest income paid to individuals and businesses during the tax year. Typically issued by banks, credit unions, and financial institutions, it is required when $10 or more in interest is paid from sources like savings accounts, bonds, or Treasury securities. The form ensures accurate income reporting for both recipients and the IRS. Businesses must provide copies to recipients by January 31 and e-file with the IRS by March 31 to remain compliant and avoid penalties, with deadlines adjusted for weekends or holidays.

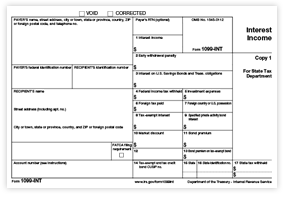

The 1099-INT is used to report interest income of $10 or more (in boxes 1, 3 and 8) from certain types of accounts, including:

The 1099-INT also captures other tax items related to interest income, such as early withdrawal penalties, federal income tax withheld and foreign tax paid.

Applicable businesses: Savings and loan associations, mutual savings banks not having capital stock represented by shares, building and loan associations, cooperative banks, homestead associations, credit unions and other financial institutions.

When to file: 1099-INT forms must be mailed to recipients by January 31, and e-filed with the IRS by March 31 each year.

NOTE: When the due date falls on a weekend or legal holiday, the form due date is moved to the next business day.

Form 1099-INT is used to report interest income from sources such as bank deposit interest, CD or time deposits interest, U.S. Savings bond or Treasury interest, tax exempt interest from municipal bonds and other related payments such as early withdrawal penalties or backup withholding. It is generally required when interest payments meet IRS reporting thresholds.

Financial institutions and other entities that pay interest income—such as banks, credit unions, and investment firms—are responsible for furnishing Form 1099-INT to recipients and filing it with the IRS.

Form 1099-INT is typically required when interest payments of $10 or more are made to a recipient. It must also be filed in cases where backup withholding or foreign tax withholding applies, regardless of the amount.

Common risks include incorrect reporting of taxable versus tax-exempt interest, failure to capture withholding amounts, and inaccurate recipient information. These issues can lead to IRS mismatches and potential penalties.

Form 1099-INT is not required for certain exempt recipients or excluded types of interest income, such as payments to corporations or tax-exempt organizations, or interest that is not subject to reporting under IRS rules. Details can be found here: https://www.irs.gov/forms-pubs/about-form-1099-int

Updated: 07/28/2026

Need to make a correction? No problem! Here's how you can get started with 1099 corrections.

Review important W-2 requirements for employee filing.

Who: Savings and loan associations and other financial institutions

When: 1099-INT forms must be mailed to recipients by January 31, and e-filed with the IRS by March 31

Where: To the IRS

Why: To report interest income of $10 or more from certain types of accounts

Free to try.

You only pay when you're ready to file.