Form 1098 Instructions & Tax Reporting Pointers

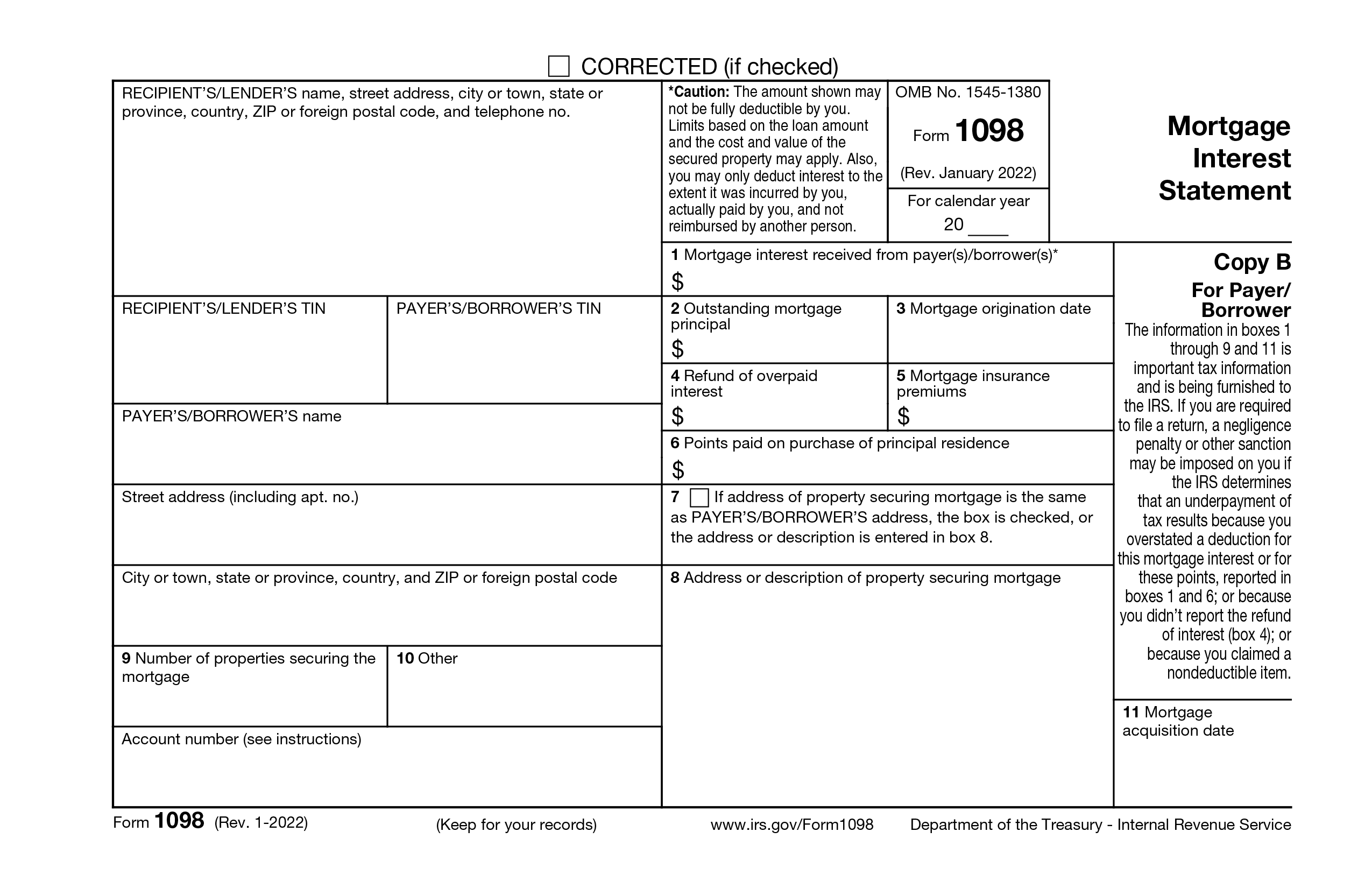

Form 1098 is an IRS information return used by lenders to report $600 or more in mortgage interest received from individuals during the tax year. It applies to each qualifying mortgage separately and helps ensure accurate tax reporting for both businesses and borrowers. Generally issued by banks and mortgage companies, Form 1098 must be sent to recipients by January 31 and filed with the IRS by March 31, with deadlines adjusted for weekends or holidays. Understanding who must file and when is key to staying compliant during tax season.

The 1098 is used to report mortgage interest (including points) of $600 or more received from an individual (including sole proprietors) during the course of trade or business. Reimbursements of overpaid mortgage interest apply, as well.

A mortgage is defined by the IRS as “any obligation secured by real property,” which generally includes land and almost anything built on it, growing on it or attached to it. Examples that are not real property include mobile homes, a boat with sleeping space that the borrower uses as a home, cooking facilities, toilet facilities. Details can be found here.

Because the 1098 applies to each mortgage, multiple mortgages require separate filings if the $600 threshold is reached for each that meets the $600 limit. The 1098 is not required for mortgage interest received from corporations, partnerships, trusts, estates, associations, or other entities that are not sole proprietors.

Applicable businesses: Banks, mortgage companies

When to file: 1098 forms must be mailed to recipients by January 31, and e-filed with the IRS by March 31 each year.

NOTE: When the due date falls on a weekend or legal holiday, the form due date is moved to the next business day.

The purpose of a 1098 form is to report certain payments made by a taxpayer—such as mortgage interest or tuition—that may be deductible or eligible for tax benefits.

Form 1098 is typically issued by the entity that receives reportable payments, such as mortgage lenders or educational institutions. The business or organization receiving the payment is responsible for reporting amounts received to both the IRS and the payer (taxpayer).

A 1098 form generally includes details such as the specified payments received by an institution, the payer and recipient identifying information, and any additional transaction details required for IRS reporting depending on the specific version of the form. This information helps the taxpayer determine eligibility for any applicable income tax deductions or credits.

1098 forms must be furnished to recipients by January 31 of the year following the reporting year, with adjustments to the next business day if the date falls on a weekend or holiday. Furnishing the recipient copy early in the year allows taxpayers adequate time to include the reported information on their income tax return for the year to determine any applicable income tax deductions or credits.

1098 forms differ from 1099 forms in that they report payments made by a taxpayer, such as mortgage interest or tuition, that may be deductible or eligible for tax benefits, while 1099 forms generally report income received by the taxpayer. Information reported on 1098 forms helps support potential tax reductions, whereas the information reported on 1099 forms is used to track potentially taxable income.

Updated: 07/28/2026

Need to make a correction? No problem! Here's how you can get started with 1099 corrections.

Review important W-2 requirements for employee filing.

Who: Banks, mortgage companies

When: 1098 forms must be mailed to recipients by January 31, and e-filed with the IRS by March 31 each year

Where: To the IRS

Why: To report mortgage interest and certain mortgage insurance premiums of $600 or more

Free to try.

You only pay when you're ready to file.