Filing Resources

Welcome to the efile4biz Filing Center, your one-stop resource for the latest 1099, W-2 and ACA forms tax-filing information affecting your business or practice.

When the One Big Beautiful Bill Act (OBBBA) was signed into law in July 2025, it introduced several changes to tax deductions for individual taxpayers.

When you're handling year-end tax forms for multiple clients, efficiency isn't a luxury — it's a necessity. Whether you're a solo accountant managing a handful of businesses or a large firm overseeing hundreds of client filings, having a secure, streamlined solution for multi-client e-filing is critical. efile4Biz — an IRS-authorized e-file transmitter — is designed to meet these demands with reliability and ease.

Read what is new at efile4Biz to make your filing easier and more efficient.

Applicable Large Employers (or ALEs) with 50 or more full-time or full-time equivalent employees must provide access to qualifying health coverage.

Before e-filing, businesses had few good options for filing 1099s, W-2s and ACA forms. Paper forms had to be ordered, filled out manually, mailed to recipients and submitted to the IRS or SSA — or handled through costly, often frustrating tax software.

As businesses conduct more activities online, the need for sophisticated data security grows. What about e-filing your 1099s and W-2s? You know the process is convenient and affordable, but how can you be sure it’s safe, too?

Working with freelancers, consultants and gig workers can offer your business flexibility and specialized skills — but only if you handle the relationship correctly from the start. Misclassifying a worker as an independent contractor instead of an employee can lead to costly fines, back taxes and legal trouble.

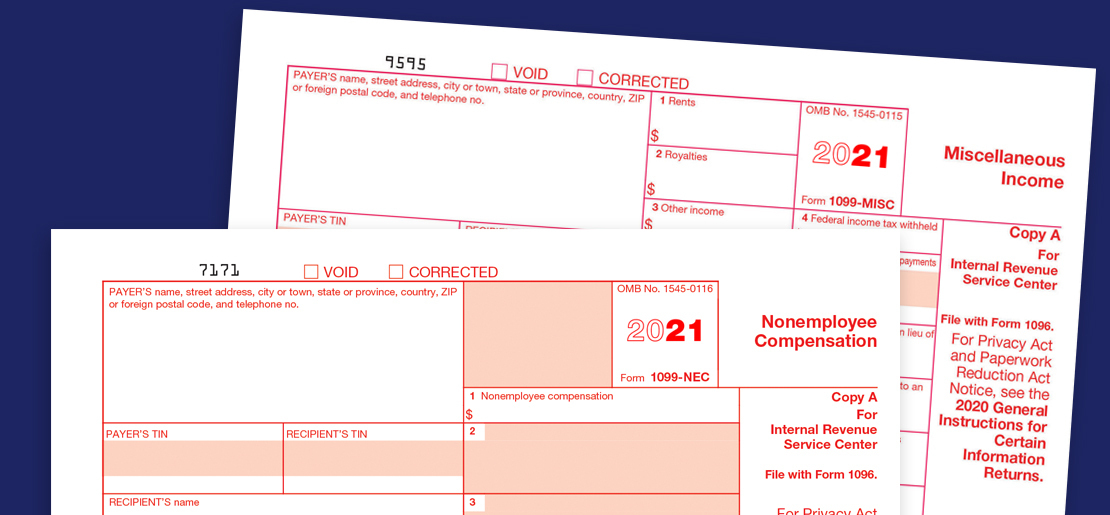

The 1099-NEC is the form that will be needed to report independent contractor payments for calendar year 2020. So who gets a 1099-NEC? Typically, this form is issued to independent contractors, janitorial services, third-party accounts and any other worker paid for services who is not on the payroll.

We live in an increasingly digital world. As we replace old, manual processes with faster, more efficient electronic options, it's not surprising that tax filing is experiencing the same shift. Businesses are no longer restricted to time-consuming and cumbersome paper filing of their taxes. Why should your business make the switch and e-file mandatory 1099 and W-2s forms?

The benefits you receive from efile4Biz are significant. For instance, we automatically notify you when your forms are accepted by government agencies. Your data is stored for use year after year so you don’t have to reenter employee and contractor information.

Rarely does a week go by that you don’t hear on the news about a security breach. Companies such as Equifax, Facebook, Google, Target and the NSA all have had significant incidents with millions of records viewed, copied, corrupted or kidnapped and held for ransom.

Relying on independent contractors to meet the needs of your business is perfectly acceptable. You may require freelancers, consultants, contractors, 1099ers, project workers, temps or specialists to supplement your staff and get the work done.

Correctly classifying your workers is more than just a paperwork exercise — it’s a critical compliance step that affects taxes, reporting obligations and liability. With federal and state agencies taking a closer look at worker classification, it’s important to understand where the line is drawn between an independent contractor and an employee.

Many businesses choose to work with independent contractors. And that’s okay. It’s perfectly legal to rely on contractors for many different services. However, the IRS has strict rules around who can be a contractor and who is an employee under the law. And the penalties for getting it wrong include having to pay back taxes and significant fines.

Working with independent contractors can offer businesses greater flexibility, specialized skills and cost savings. But to stay compliant, it's essential to understand how this type of work relationship differs from traditional employment.

When it comes to the safe handling and storage of sensitive tax data, businesses and tax preparers can’t be too cautious. The risk of hacking and cyber fraud is always present, requiring airtight procedures, the latest technological advances and careful screening of vendors.

With news of data breaches and identity theft dominating the headlines, you may question the security of e-filing. How can you be certain the sensitive information of your independent contractors and employees – including Social Security numbers and tax IDs — doesn’t fall into the wrong hands?

You've probably heard of working and storing information in the cloud, but did you know you can file your 1099s, W-2s and ACA forms in the cloud, too? That's right! Rather than muddle through manual processes or restrict yourself to installed software, you can manage your annual tax filing quickly and easily in the cloud. With the tax-filing season right around the corner, now is the time to explore all the perks of cloud-based e-filing.

As a small business owner, you most likely rely on digital payment services through third party networks like Paypal®, Venmo® or Zelle® to pay certain contractors and expenses.

As an accountant or bookkeeper, you rely on the information your clients provide to prepare 1099-NEC forms. If this information isn’t complete or accurate, there may be complications or IRS penalties. Send an engagement letter to your clients so they know what to expect from your firm, including the details needed for the prompt filing of their forms.

No longer just the focus of sci-fi thrillers or global corporations, cyber security has entered the mainstream. Today, if you conduct any sort of business online, you need to care about data security.

If you have employees, you also have payroll responsibilities. In addition to properly compensating your employees, you must withhold certain taxes and maintain accurate records.

Are you doing enough to cut your tax burden down to size? Understand the deductions available to your small business and how to report them to reduce your taxable income.

When your business is affected by a disaster, there are many agencies and programs ready to provide aide to assist in your recovery.

In February 2023, the IRS issued a new regulation mandating electronic filing for entities that file more than 10 information returns in a calendar year. This long-anticipated reduction in the e-filing threshold, which was previously set at 250 forms, was authorized as part of the Taxpayer First Act (TFA) of 2019.

It’s almost here again – tax-filing “crunch time.” The time of year when accounting professionals and small business owners burn the midnight oil gathering information and completing tax forms. Stress levels can be high, but there are steps you can take to save your sanity.

In today’s increasingly digital world, it should come as no surprise that electronic tax filing is replacing old, manual processes. Businesses are no longer restricted to time-consuming and cumbersome paper or software-driven tax filing. Instead, they are turning to reputable, IRS-authorized e-file providers like efile4Biz.com to file taxes online and save valuable time and money.

For years now, you’ve handled your annual 1099 and W-2 reporting the same, old way – manually via paper forms or with software. You’re aware of e-filing, but you have your reservations. E-filing isn’t for everyone, you say. Every business owner’s perspective is different, but the reasons for resistance tend to fall under a few key areas.

As a business owner or tax preparer, you know that e-filing your 1099s, W-2s and new 1095s with efile4Biz.com is fast and efficient. Simply enter (or import) your recipient and form data online and we handle the rest – printing and mailing copies to your recipients, filing forms directly with the IRS or SSA, and sending notifications for confirmation.

It’s called a TIN – and it’s an essential number when filing W-2s, 1099s and ACA forms. A TIN, or Taxpayer Identification Number, is simply an individual’s Social Security number (SSN), or the Employer Identification Number (EIN), or EIN, for a business entity.

When you’re handling lots of detailed information with 1099 and W-2 tax forms, you’re bound to make mistakes. But correcting them is easier than ever with our all-inclusive service.

The IRS introduced the 1099-NEC in 2020, which changes how business owners and tax professionals handle certain types of tax reporting. Basically, the Form 1099-NEC replaced Form 1099-MISC for reporting nonemployee compensation (in Box 7), shifting the role of the 1099-MISC for reporting all other types of compensation.

The IRS has released Form 1099-NEC, replacing Form 1099-MISC with box 7 data. In this article, we discuss the purpose of the two forms, their differences and filing requirements for each.

Recruiting and hiring top employees for your small business can be challenging — especially when you’re competing against large, thriving companies who can offer more financial incentives.

Struggling to keep on top of required labor law postings? Consider this catchy 5-letter prompt to remember what, when and where to post: Post the Proper Posters Prominently, and Protect Them.

They say one of the best-run organizations in the world is the U.S. Army — largely due to its leadership, structured environment and strict rules. While the Army has a rule book dictating nearly everything, your business probably doesn’t need anything that drastic. A well-thought-out employee handbook should do the trick — one that clearly sets expectations.

Everyone needs time off from work once in a while to take care of personal matters, relax or recover from illness. Offering paid time off to employees provides a desirable benefit that can help you attract and retain good people. But what is the best way to track and manage your employee time off policy?

With this year’s tax-filing deadlines looming large, many employers are feeling the pressure of the new reporting requirements under the Affordable Care Act (ACA). In addition to annual 1099 and W-2 filing, applicable large employers (ALEs) with 50+ employees must report healthcare coverage information to employees and the IRS through the 1095-C (and transmittal form 1094-C).

Free to try.

You only pay when you're ready to file.